How I Cut Rehab Treatment Costs Without Sacrificing Care

Rehabilitation treatment can hit your wallet hard—trust me, I’ve been there. After my own recovery journey, I realized how easily costs add up: therapy sessions, equipment, travel, and time off work. What started as a healing process almost became a financial nightmare. But through careful analysis and smart choices, I found ways to reduce expenses without cutting corners on quality. This is my story—and how you can make rehab more affordable, too. The path to recovery should not come at the cost of long-term financial stress. With the right strategies, it’s possible to protect both your health and your savings.

The Hidden Price of Recovery: Why Rehab Costs Surprise Most People

Rehabilitation is often seen as a necessary step toward regaining strength, mobility, and independence after an injury or surgery. Yet for many, the financial burden that accompanies this journey comes as a shock. Most patients assume their insurance will cover the majority of rehabilitation expenses, only to discover later that co-pays, deductibles, and uncovered services quickly accumulate. The reality is that rehab involves more than just therapy sessions—it includes diagnostic tests, medical equipment, transportation, and often time away from work. These indirect costs are frequently overlooked but can significantly strain household budgets.

One of the biggest challenges in managing rehab costs is the lack of price transparency in healthcare. Unlike other industries where prices are clearly listed, medical services often come with vague billing codes and inconsistent charges. A single physical therapy session might cost $120 in one clinic and $220 in another—without any visible difference in care quality. Patients rarely receive detailed estimates upfront, making it difficult to plan or compare options. This opacity can lead to unexpected bills weeks or even months after treatment, sometimes resulting in collections or damaged credit if not addressed promptly.

Another factor contributing to high costs is the frequency and duration of treatment. Many rehabilitation programs require multiple sessions per week over several weeks or months. While medically justified, this schedule multiplies expenses—especially when combined with travel, parking, and lost wages. For those living in rural areas or without reliable transportation, the added cost of commuting or staying near a facility can be substantial. Even seemingly minor charges, such as fees for missed appointments or equipment rentals, can add up over time. Understanding these components is the first step in taking control of rehab spending.

It’s also important to recognize that not all providers are created equal in terms of insurance networks. In-network clinics typically charge lower rates and require smaller co-pays, while out-of-network providers may leave patients responsible for a much larger portion of the bill. Without careful verification, patients may unknowingly receive care from an out-of-network therapist, leading to surprise charges. By asking the right questions early—such as whether a provider is in-network, what services are covered, and what the estimated out-of-pocket cost will be—individuals can avoid many of these pitfalls. Awareness is power when it comes to managing healthcare expenses.

My Wake-Up Call: When Medical Bills Started Piling Up

I entered rehabilitation with confidence. I had health insurance through my employer, a referral from my doctor, and a treatment plan that seemed straightforward. My therapist was experienced, the clinic was well-reviewed, and I was committed to following the prescribed routine. I assumed my financial responsibility would be limited to a standard co-pay per session. But within a few weeks, that assumption began to unravel. Bills started arriving—not just monthly statements, but detailed invoices with charges I didn’t recognize. Some services were labeled as “non-covered” or “exceeding allowable fees,” and my insurance had only paid a fraction of the total.

The emotional toll was just as heavy as the financial one. I felt anxious every time the phone rang, worried it was a collection agency. I began skipping sessions—not because I didn’t need them, but because I couldn’t afford another $80 co-pay on top of parking and gas. The irony wasn’t lost on me: I was healing my body, but my mental well-being was deteriorating under the weight of mounting debt. I started dreading medical mail, avoiding phone calls from billing departments, and lying awake at night wondering how I’d cover the next bill. Recovery, which should have been a hopeful process, had become a source of constant stress.

The turning point came when I received a bill for over $400 for a single month of therapy—nearly double what I had expected. That’s when I decided to take action. I requested a full itemized statement from the clinic and a detailed explanation of benefits from my insurer. I spent hours on the phone, asking questions, clarifying coverage, and challenging charges that didn’t make sense. What I discovered was eye-opening: some services were billed at out-of-network rates even though the clinic claimed to be in-network. Other charges were for “facility fees” that weren’t clearly explained during intake. I realized I had been passive in managing my care—and that needed to change.

From that moment on, I shifted my mindset. I stopped seeing myself as just a patient and began thinking like a consumer. I started tracking every expense, asking for cost estimates before each appointment, and researching alternative providers. I learned to read medical bills line by line and to appeal denied claims with documentation. It wasn’t easy, and it took time, but each small step gave me more control. Most importantly, I didn’t let financial fear stop my recovery. Instead, I used it as motivation to become more informed, more proactive, and ultimately, more empowered in managing my healthcare.

Mapping the Real Cost: A Practical Breakdown of Rehabilitation Spending

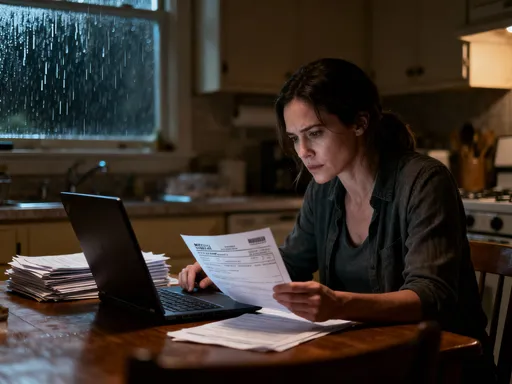

To regain control of my finances, I created a simple but effective cost-tracking system. I listed every expense related to my rehabilitation, no matter how small. This included therapy sessions, transportation, parking, medical supplies, and even the value of time taken off work. By categorizing each cost, I could see exactly where my money was going. What I found was surprising: while therapy sessions made up the largest portion of spending, indirect costs like gas, tolls, and missed work hours added up to nearly 30% of my total rehab budget. These were expenses I had initially dismissed as minor, but over time, they had a significant impact.

Direct medical costs included the price of each therapy visit, any diagnostic imaging ordered during rehab, and fees for specialized equipment such as braces, resistance bands, or walking aids. Some of these items were covered by insurance, but many required upfront payment with partial reimbursement later—if at all. I also discovered that facility fees, which are separate from the therapist’s fee, were being charged at each visit. These fees, often labeled as “clinic service charges,” can range from $20 to $50 per session and are not always included in insurance estimates. Without clear disclosure, patients may not realize they’re being charged until the bill arrives.

Indirect costs were harder to quantify but equally important. Each therapy session required at least an hour of travel time, during which I couldn’t work or handle household responsibilities. For self-employed individuals or those without paid leave, this lost income can be substantial. I calculated that I was losing nearly $200 per month in potential earnings just from time spent in transit and at appointments. Parking fees, tolls, and vehicle maintenance added another $75 per month. These figures might seem small individually, but over a 12-week program, they totaled over $1,000—money that could have been used for other necessities.

Another factor I hadn’t considered was the cost of treatment length. My initial plan was for eight weeks of therapy, but due to slow progress, it extended to 14 weeks. That six-week extension added nearly $600 in additional therapy fees alone, not counting the extra travel and time costs. I learned that treatment duration is not always predictable, and longer recovery times mean higher expenses. This made me realize the importance of setting a budget with a buffer for unexpected extensions. It also highlighted the value of early progress tracking and open communication with my therapist about goals and timelines.

By mapping out these costs, I gained clarity and control. I could identify areas where I might save—such as switching to a closer clinic or using telehealth options—and make informed decisions. This level of awareness didn’t eliminate the costs, but it removed the element of surprise. Instead of reacting to bills after they arrived, I could anticipate them and plan accordingly. That shift—from reactive to proactive—was one of the most empowering changes in my entire recovery journey.

Smart Substitutions: Lower-Cost Alternatives That Actually Work

One of the most effective ways I reduced my rehab costs was by finding lower-cost alternatives that didn’t compromise care. The first change I made was switching from in-person sessions to telehealth for certain parts of my therapy. My clinic offered virtual appointments for exercise review and progress check-ins, which eliminated travel time and costs. While hands-on treatment still required in-person visits, about 40% of my sessions could be done remotely. This simple adjustment saved me over $300 in gas, parking, and tolls over the course of my program.

I also explored community health centers and nonprofit rehabilitation programs. These organizations often offer sliding-scale fees based on income, making therapy more affordable for those with limited budgets. I found a local clinic affiliated with a university physical therapy program that provided supervised treatment at a fraction of the cost. While the therapists were students, they worked under licensed instructors and followed evidence-based protocols. The quality of care was excellent, and the savings were significant. For maintenance-phase exercises, this option was ideal.

Another strategy was scheduling sessions during off-peak hours. Some clinics offer discounted rates for early morning, late afternoon, or weekend appointments to fill unused time slots. I shifted two of my weekly sessions to early evenings and received a 15% reduction in fees. It required some adjustment to my routine, but the trade-off was worth it. I also asked if bundled payment options were available—paying for a set number of sessions upfront at a discounted rate. This not only lowered the per-session cost but also gave me a clear end date, which helped with motivation and financial planning.

At home, I implemented a structured exercise routine under my therapist’s guidance. Using a printed plan and instructional videos, I performed daily stretches and strength exercises that complemented my in-clinic work. My therapist reviewed my progress during virtual check-ins and adjusted the plan as needed. This hybrid model reduced the number of required in-person visits without affecting outcomes. In fact, studies have shown that home-based rehabilitation, when properly supervised, can be just as effective as full clinic attendance for many conditions. The key is consistency and clear communication with your provider.

Negotiating Like a Pro: How to Talk to Providers and Insurers

One of the most powerful tools I discovered was the ability to negotiate medical bills. Most people don’t realize that healthcare prices are not fixed—there is often room for discussion, especially if you’re paying out of pocket or facing financial hardship. My first step was requesting an itemized bill, which broke down each charge. This allowed me to identify duplicate fees, incorrect codes, or services I didn’t receive. When I spotted a $45 “facility fee” listed twice for the same visit, I called the billing office and had it corrected.

I also learned to ask for discounts. When I explained my financial situation to the clinic’s billing coordinator, they offered a 20% reduction if I paid the balance in full within 30 days. Other clinics may offer payment plans with no interest, which can make large bills more manageable. I made sure to get any agreement in writing and kept records of all payments. Persistence was key—sometimes I had to call multiple times or speak with a supervisor to get a favorable response. But each time I advocated for myself, I saved money.

Dealing with insurance required a different approach. I reviewed my explanation of benefits carefully and compared it to the provider’s bill. When discrepancies appeared, I filed appeals with supporting documentation from my doctor. One claim had been denied because the service was labeled as “not medically necessary,” but my physician wrote a letter explaining its importance to my recovery. The appeal was successful, and my reimbursement increased by $180. I also called my insurer’s customer service to clarify coverage before scheduling new services, which helped me avoid future denials.

The most important lesson was that silence guarantees no change. If you don’t ask, you won’t receive. Whether it’s a discount, a payment plan, or a corrected charge, the system only responds when patients speak up. Being polite but persistent, organized and informed, transformed me from a passive recipient of care to an active participant in my financial well-being.

Building a Financial Safety Net: Planning Ahead for Future Treatments

After my experience, I knew I had to prepare for the future. I started setting aside a small amount each month into a dedicated medical savings fund. Even $50 a month adds up to $600 a year—enough to cover a significant portion of unexpected rehab costs. I also opened a Health Savings Account (HSA), which allowed me to save pre-tax dollars for qualified medical expenses. The triple tax advantage—tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical use—made it an ideal tool for long-term healthcare planning.

I reviewed my insurance plan annually during open enrollment, comparing coverage for physical therapy, specialist visits, and out-of-network care. I chose a plan with lower deductibles and better rehab coverage, even if the monthly premium was slightly higher. In the long run, the savings on out-of-pocket costs outweighed the extra premium. I also added secondary insurance through my spouse’s employer, which helped cover gaps in primary coverage.

Budgeting for planned procedures became part of my financial routine. If I knew surgery or rehab was on the horizon, I adjusted my spending months in advance—cutting non-essentials, increasing savings, and arranging flexible work schedules. This proactive approach reduced last-minute stress and gave me peace of mind. Recovery should be focused on healing, not on worrying about money.

The Bigger Picture: Balancing Health and Financial Well-Being

Looking back, I realize that true recovery isn’t just about physical healing—it’s about achieving financial stability, too. The stress of unmanaged medical bills can delay healing, increase anxiety, and affect relationships. By taking control of my rehab costs, I protected not only my savings but also my mental and emotional health. Smart financial decisions didn’t compromise my care; they enhanced it by allowing me to stay consistent and committed without fear of debt.

Rehabilitation is an investment in your future self. When approached with planning, awareness, and confidence, it doesn’t have to come at an unbearable cost. The strategies I used—tracking expenses, seeking affordable alternatives, negotiating bills, and preparing in advance—are accessible to anyone. They require effort and persistence, but the payoff is worth it: the ability to heal without financial regret.

Every woman managing a household, caring for family, and balancing work deserves to feel secure in her health and finances. You don’t have to choose between quality care and a stable budget. With the right tools and mindset, you can have both. Recovery is not just about returning to where you were—it’s about emerging stronger, wiser, and more empowered in every aspect of life.